The Insurance Pros Blog:

Your Resource for Smart Coverage

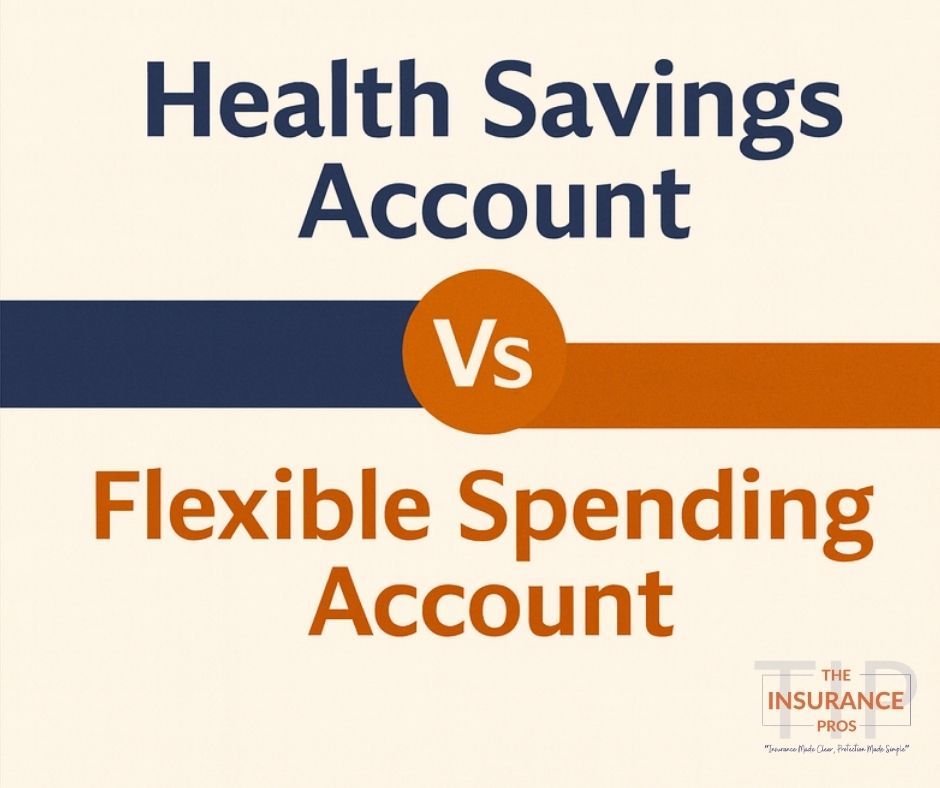

Ever stare at your benefits enrollment screen (or that 52-page HR doc) and think, “Did I just stumble into an episode of Alphabet Soup: Insurance Edition?” HSA? FSA? HDHP? IRS? It feels like trying to solve a Rubik’s Cube while wearing oven mitts. But don’t stress—I’ve got your back. Let’s unpack two of the most confusing and most valuable players in your health-and-money playbook: the Health Savings Account (HSA) and the Flexible Spending Account (FSA). Here’s the deal: both are awesome. But only one may be the MVP for you. So, What Are They? Both HSAs and FSAs let you stash away pre-tax dollars to pay for qualified medical expenses. Think of them as your personal medical piggy banks—for co-pays, prescriptions, dental work, and even that chiropractor you’ve been low-key avoiding. But they’re not twins. There are a few key differences—like who qualifies, how they’re managed, and what happens if you don’t use the funds. HSA vs. FSA: Let’s Break It Down

Hey Bosses: The “One Big Beautiful Bill” Is Here to Shake Up Your Health Plan. Let’s Not Get Played.

Hey, business owners — While you’ve been out here literally minding your business, Congress slipped a plot twist into your benefits strategy: the One Big Beautiful Bill. Spoiler alert — it’s here to flip how you support your people and how you spend your dollars. If you’ve got a team — or you want to offer real-deal benefits without setting fire to your profits — keep reading. We’re about to unpack what just happened and how to play it smarter than Uncle Sam thinks you will. CHOICE Arrangements & ICHRAs: Your Exit From the Group Plan Hamster Wheel For years, small business owners have been stuck: rising premiums, rinse, repeat, rage scream. This new bill says: “You don’t have to keep doing that.” Say hello to Individual Coverage HRAs (ICHRA) and “CHOICE arrangements.” Fancy names, simple shifts: 👉 Instead of overpaying for a group plan, reimburse your employees (tax-free!) when they buy their own coverage through the Marketplace. 👉 They may get a subsidy. You may get a tax break. And sanity may just return to the benefits process. If you’ve got fewer than 50 employees, this could be your benefits glow-up. Just know — you can’t CashApp them their premium and call it a day. The IRS will not be amused. Follow the rules or risk the consequences. HSAs Got a Mini Makeover You already know I’m Team HSA — tax-free money for healthcare? Sign me up. And now? The updates are actually helpful: ✔️ Spouses can both make “catch-up” contributions to the same HSA. ✔️ Rolling leftover FSA or HRA funds into your HSA is easier. ✔️ Paying for direct primary care? That now counts as an eligible HSA expense. ✔️ More Bronze plans now qualify for HSA use. Translation: HSAs are now easier to use and more valuable. If you offer one, shout it from the rooftops. If you don’t — maybe this is your sign. PBMs Just Got Put on Watch The bill also takes a swipe at shady Pharmacy Benefit Manager (PBM) practices under Medicaid. It doesn’t touch commercial plans (yet), but if you’re self-funded or deal with a PBM? Eyes open. States love to follow the money — and each other. So, What’s a Smart Boss Supposed to Do? Great question: ✅ Still offering a group plan? Run the numbers. If it’s not working anymore, it’s time to consider a hybrid plan, level-funded option, or ICHRA. ✅ No plan yet? CHOICE might be your moment. Do something solid for your team without incinerating your margins. ✅ Already have HSAs? Educate your crew. Don’t let them miss out on tax-free savings. Tell them what’s new. ✅ Call your broker (hi, that’s me). This is not the year to DIY benefits. I’ll read the fine print, review your costs, and make sure you're squeezing every dollar the legal way. TL;DR? Congress keeps remixing the benefits rulebook — but smart business owners don’t get caught sleeping. You don’t have to be the expert here. That’s my lane. Yours is to keep your team thriving, your profits intact, and your accountant off blood pressure meds. Still wondering: ❓“Is my group plan even worth it?” ❓“Should I switch to an ICHRA?” ❓“Could an HSA actually help my team save money?” Hit reply. Let’s run the math before your next renewal hits like a plot twist you didn’t see coming. — Carmen Londono The Insurance Pros

In case it got buried under everything else happening in the world — the “One Big Beautiful Bill” just passed into law, and it’s about to reshape how millions of Americans get and keep their health coverage. Don’t worry — I’ve waded through the 1,000+ pages so you don’t have to. Here’s what actually matters for you, especially if you rely on Medicaid, Marketplace coverage, or tax credits to make health insurance make sense. What’s Changing? Medicaid Just Got Stricter States now have to check eligibility more often — meaning more income verifications, address confirmations, and general paper-chasing. If you’re on Medicaid, don’t be surprised if the mail starts piling up with requests for proof. Here’s the kicker: Miss a deadline, and you could lose your coverage — even if you technically still qualify. Marketplace Subsidies = New Rules, Too Buying your plan on Healthcare.gov or your state’s exchange? Get ready for more eyes on your income estimates. The IRS now has stronger claws to take back your advance premium tax credits if you end up making too much. That old “oops, I earned a little more” cushion? Gone. So if your income shifts? Report it ASAP. It could save you a major headache (and bill) come tax time. Some Bright Spots for Employers and HSAs If you’ve got an HSA with your job — or you are the job and run a small business — this law has a few silver linings: ✔️ More flexibility with HSAs ✔️ New credits for certain employer arrangements ✔️ Easier integration with individual plans Translation: if you play your cards right, you can save tax-free money for medical expenses — and help your people do the same. For Immigrants & Certain Families — Read Closely This law also comes with tighter rules around undocumented immigrants and federal funding for certain procedures for minors, including gender-affirming care under Medicaid/CHIP. If this impacts your household , be especially mindful of eligibility letters or shifts in your benefits. So What Should You Do Now? Check your mail. Seriously. Open it. Respond. There are deadlines. Report income changes quickly. Got a raise? New job? More hours? Log in and update your info. Keep everything organized. This is your season to be that person: save letters, track what you send, and screenshot receipts. Reach out for help. You don’t have to figure this out alone. I do this every day and would be honored to help you sort through what it means for your family. The Big Picture? More paperwork. More hoops. But also — more ways to protect yourself if you stay on top of it. Congress may move the goalposts, but you’ve still got power. Let’s keep your coverage locked in, your paperwork tight, and your tax surprises at zero. Need help? 📬 Hit book a chat. No question is too small — and no one should have to navigate this mess alone. Stay covered. Stay sharp. We’ve got this. — Carmen Londono The Insurance Pros 💙 P.S. Know someone who could use this info? Forward it. We keep each other safe by staying informed.

Your vision plan? It’s out here doing more for your wallet than you probably realize — if you actually use it. Here’s the tea: the average person pays about $8 a month for individual vision coverage. That’s literally two fancy iced coffees, a sad half sandwich, or one of those mystery subscriptions you forgot to cancel. But that $8? It does the most: Eye exam? $10 copay (usually). Without it, you’re paying $50–$100 easy. Frames or lenses? Most plans toss you $150 a year to spend. That’s real money back in your pocket (and better glasses on your face). So yes — your vision plan is basically printing money if you actually use it. And don’t get me started on what else an eye exam can catch: high blood pressure, diabetes, all kinds of sneak attacks on your health. It’s not just about seeing the TV better — it’s about seeing life clearer. So be for real: when’s the last time you got new glasses you actually liked? Or went to your eye doc without side-eyeing the bill? ✨ If you’re an employer: Vision is one of the cheapest, easiest ways to show your people you care — and they love it. Tiny perk, big loyalty. Moral of the story: If you’ve got the benefit — use it. Healthy Vision Month is your sign. Stop squinting at the world when your insurance is begging you to fix it. Got questions about adding vision coverage for your crew? Or whether you’re still getting the best bang for your buck? Slide into my inbox.

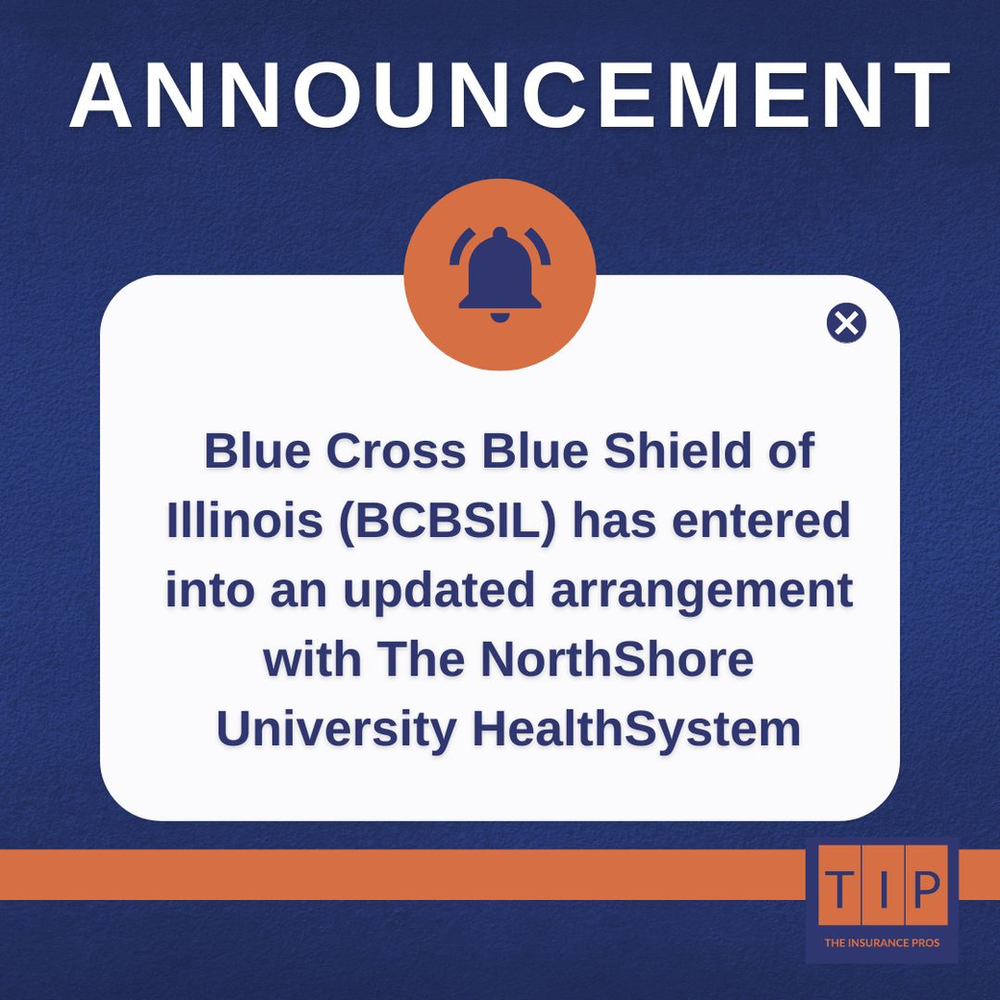

Big news, friends — Illinois just made it Facebook Official. We’re breaking up with Healthcare.gov, and starting in 2026, we’re running our own health insurance marketplace. If you rely on the ACA Marketplace, hate glitchy websites, or just want to know what’s happening with your coverage (before it happens to you), grab a seat. I’ve got you. The Breakup Is Real (And Kind of a Glow-Up) Welp, it’s happening. After years of paying the feds to host our Marketplace while they ran the show, Illinois finally said: “We got this.” Starting with the 2026 plan year , you’ll shop for coverage at GetCovered.Illinois.gov . Bookmark it now, thank yourself later. This shift means: Local control 💪🏽 Tailored plan options 🧩 Real accountability 👀 Because honestly? Who knows what Illinoisans need better than... Illinois? Meet the New BFF: Get Covered Illinois Here’s what you can expect when the new platform rolls out November 1, 2025: 🛍️ Browse First, Commit Later Shop and compare plans before creating an account. Knowledge is free — and so are the quotes. 💸 Financial Help Isn’t Going Anywhere Subsidies (like tax credits and cost-sharing reductions) are still available. They’ll just be calculated locally instead of federally. 🧑🏽💻 Real Help, Not Robocalls Whether it’s a Zoom call, text, or in-person meeting, I’ll be here to translate deductible-speak into plain English — no decoder ring required. 🧭 One Site. One Login. No Bouncing Around. ACA plans and Medicaid will now be under one roof. It’s about time. But Let’s Be Real: Transitions Come with Glitches New platform = new hiccups. Expect some: Frozen pages Broken links Confused screens Open Enrollment chaos (we’ve seen it before) That’s why having a broker matters more than ever . I know what “affordable” actually means. I know how to avoid those “looks-good-but-isn’t” plans. I’ll help you keep your coverage clean and your stress low. A Bit of Policy Grit for the Nerds (Love You) This isn’t just a tech rebrand. House Bill 579 , signed by Governor Pritzker, makes this official and gives the state more power to: Prevent shady premium hikes Regulate plans that actually fit our needs Translation? We’re done watching our premiums play Jenga while nodding politely. What You Should Do Right Now 🗓️ Save the Date : November 1, 2025 = new open enrollment 🔗 New URL : GetCovered.Illinois.gov 📲 D o n’t DIY This : Call me, Zoom me, text me. I’ll walk you through it. FAQs (Because You’re Smart Like That) Q: When is the switch happening? A: For 2026 plans. Open enrollment starts November 1, 2025. Q: Will I still get tax credits or subsidies? A: Yes — they’ll just be handled through the new Illinois platform. Q: Do I need a broker? A: Technically no. Realistically? Yes. A licensed broker (hi, that’s me 👋🏽) helps you avoid expensive mistakes and bad coverage choices. TL;DR? Illinois is building its own table. It might get bumpy — but it’s going to be better. And you don’t have to go it alone. 📣 You deserve insurance that makes sense, not one that makes you cry into your coffee. Let’s get you covered — clearly, confidently, and without the chaos. — Carmen Still out here Covering Your ASSets with heart, hustle, and plain-language policy talk P.S. Se habla español. 💬

Protect Yourself Before a Scammer Turns Your Life Into Their Side Hustle.

This month, while the Humboldt Park flags wave high and the streets fill with the rhythm of bomba and salsa, I’m taking a moment to honor someone whose name may not come up during Puerto Rican Pride Weekend—but should. Dr. José Celso Barbosa wasn’t just a trailblazer in medicine—he helped plant the seeds for something we now take for granted: employer-based health insurance . Yes. A Black Puerto Rican physician from Bayamón is credited with developing one of the earliest systems where employers pooled funds to provide healthcare for their workers. Let that sink in. 👨⚕️ Meet Dr. José Celso Barbosa First Puerto Rican to earn a medical degree in the U.S. (University of Michigan, Class of 1880) Faced racial discrimination both abroad and at home Established cooperative health models in Puerto Rico—essentially early employer-sponsored care Believed access to healthcare wasn’t charity. It was justice. He imagined a world where working people didn’t have to choose between a paycheck and a doctor visit. And he built toward it. 🏙 Why His Legacy Still Hits in 2025 Today, more than 150 million Americans receive health coverage through their employer. Whether you love or side-eye the system, the truth is: for many, that coverage is a lifeline. For me, running an insurance agency rooted in advocacy, Barbosa’s work feels personal . Every time I help a business owner protect their team—or guide someone through job loss and COBRA—I’m reminded that this work goes beyond spreadsheets. It’s about dignity. He didn't just advocate. He organized. And in 2025, we need more of that. 💡 3 Small Ways to Carry His Legacy This Month Look at your benefits through a justice lens. Are your part-timers and hourly staff just as protected as your full-timers? Talk to your team. Don’t just send a PDF. Educate them. A confused employee is a vulnerable one. Celebrate Puerto Rican Pride Weekend with intention. Support local Boricua-owned businesses. Learn the stories behind the flags. 🎯 Why This Matters to Me—and Maybe to You Employer-based insurance didn’t start in a corporate boardroom. It started with a Puerto Rican doctor who believed care should be a right, not a privilege. So this June, while we dance in the streets of Chicago, I’ll be thinking about the quiet power of legacy—the kind that shows up in EOBs, provider networks, and someone finally getting the prescription they need. To Dr. Barbosa : Gracias por todo. And to you—whether you’re a business owner, an HR lead, or just someone trying to make sense of this benefits maze—I'm here when you're ready. Carmen ✨ PS: Chicago’s Puerto Rican Pride festivities run June 12–15 in Humboldt Park. Go. Eat well. Dance hard. And bring sunscreen.

Why Your Insurance Bill Looks Disrespectful and How to Fight Back

As women, we’re out here building legacies—owning 40% of U.S. businesses, leading households, breaking barriers, and doing it all with grit and grace. But behind the scenes? 🚨 We’re underfunded. ⚡ We face higher financial risks. 💸 We carry less life insurance. 😬 And almost half of us small biz owners will face a lawsuit at some point. Let that sink in. We’re building empires—without a safety net. What We’re Seeing in the Field As an insurance expert, I’ve seen too many women thriving publicly, while quietly skipping out on the financial protection they need: Not enough liability coverage. No buy-sell agreement in place. Zero disability insurance. Life insurance that wouldn’t even cover the funeral. It’s not because we don’t care—it’s because no one sat us down and made it make sense. That’s why I started The Insurance Pros. Because insurance shouldn’t be a guessing game. Especially for women who are doing the most. How to Play Yourself in 3 Easy Steps (Don’t Do These) Skip coverage to “save” money. Spoiler alert: one ER visit or lawsuit could cost 50x more than a monthly premium. Assume your current policy has your back. If you haven’t reviewed your coverage lately, chances are it’s outdated—or incomplete. Think life insurance is “extra.” If your family or business depends on you, then you are essential—protect accordingly. So What Do We Do? We Move Like the Legends Before Us This Women’s History Month, let’s honor the women who paved the way—by taking ownership of our future. ✔️ Protect what you’ve built. From your LLC to your babies, they all deserve security. ✔️ Know your worth. You’ve worked too hard to leave your assets exposed. ✔️ Lead boldly. Insurance isn’t about fear—it’s about freedom to take bigger, smarter risks. Final Word: Don’t Just Build. Fortify. Whether you’re a solopreneur, CEO, or caregiver with a side hustle—this is your moment. Don’t leave what you’ve built unprotected. Because empowered women don’t just lead. They shield their empire, too. 👋 Ready to Talk Coverage That Actually Works for You? Let’s make sure your business, your family, and your vision are covered. 💬 Book a free strategy session with Carmen today at www.insurepros.net .

Let’s go ahead and say the thing out loud: Men don’t always talk about their health. Whether it’s ego, upbringing, fear, or just not knowing where to start—far too many men delay care, skip checkups, and brush off symptoms like they’re just “tired.” And you know what? That silence? It’s costing lives. June is Men’s Health Awareness Month , which means now is the perfect time to shine a light on the issues that don’t always make it to the group chat—but should. Because “I’m fine” is not a health strategy. And prevention is still better (and cheaper) than crisis mode. Why Men’s Health Deserves the Spotlight Let’s look at the facts: Men die 5 years earlier than women, on average They’re more likely to die from heart disease, cancer, and suicide And yet… they’re less likely to go to the doctor If that math ain’t mathing for you either, welcome to the club. But here’s the good news: A few intentional steps—not major overhauls—can change the game for the men in our lives. 3 Health Moves Every Man Should Make This Month 1. Book the Damn Checkup Seriously. No badge of honor comes from ignoring your blood pressure or that nagging pain in your back. Even a basic physical can detect early warning signs for everything from diabetes to prostate issues. And if you're over 40, get that cholesterol checked . You can’t fix what you won’t face. 2. Don’t Sleep on Mental Health Men are conditioned to “man up” and bottle things up—but depression, anxiety, burnout, and trauma don’t care about your masculinity. Therapy is strength. Vulnerability is power. If you’ve been feeling off, talk to someone. There’s no shame in healing. 3. Know What Your Insurance Covers Many preventive screenings are 100% covered under health insurance. That means free annual checkups, screenings, and more—no excuses needed. If you're unsure what your plan covers, let me help. Seriously. One quick review could save your life and your wallet. 💡 Carmen’s Take Men’s Health Month isn’t about scare tactics. It’s about making health a habit , not an emergency. Whether you’re a man reading this or someone who loves one, use this month as a gentle nudge: check in, check up, and take action . Because we need our brothers, fathers, partners, friends, and sons to be here—not just pushing through pain like it’s noble. What You Can Do Right Now ✔️ Haven’t had a checkup in over a year? Schedule it. ✔️ Not sure what your coverage includes? Reply “Review mine” and I’ll walk you through it. ✔️ Know a man who needs this message? Forward it with love (and maybe a side-eye). You matter. Your health matters. Let’s normalize prevention, pride in wellness, and asking for help when you need it. Not just this month—but always. With heart, Carmen The Insurance Pros

Welcome to The Insurance Pros Blog—where we break down what your policy really means (without giving you a headache). I'm Carmen Londono , founder of The Insurance Pros. With over two decades in the insurance world, I’ve seen firsthand how overwhelming policies can be—especially for business owners trying to make smart, confident decisions without drowning in fine print. That’s exactly why I created this blog: to make insurance make sense. No jargon. No nonsense. Just the guidance you need, delivered like a conversation with your smartest (and sassiest) friend in the biz. What You’ll Get from This Blog ✅ Bite-Sized Insurance Tips Cut through the clutter with clear, digestible tips that help you make better decisions fast. ✅ Real Talk for Business Owners Understand how to protect your business, your employees, and your profits without falling into common coverage traps. ✅ Timely Industry Trends & Updates Stay ahead of the curve with insights that impact your bottom line—from policy changes to emerging risks. ✅ A Dash of Humor (Because Why Not?) Let’s face it—insurance can be dry. But we keep it lively around here, because learning should never be boring. Who This Blog is For If any of the following sound like you, bookmark us now: You’re a small business owner trying to offer employee benefits without breaking the bank. You’re an HR manager who wants to keep your team informed without putting them to sleep. You’re a self-employed professional who needs flexible coverage that actually fits your life. You’re just plain tired of Googling insurance terms and ending up more confused than when you started. Let’s Cover Your Assets (The Right Way) Insurance is personal. It’s also business-critical. The more you know, the better you can protect what you’ve built. That’s where we come in. Ready to take control of your coverage? 👉 Book a Free 15-Minute Insurance Check-In We’ll review what you have, identify any gaps, and make sure your coverage is working for you—not against you. Don’t miss a post. Stay in the know with expert tips, insider insights, and Carmen’s no-nonsense approach to all things insurance. 📬 Subscribe to Our Blog Update s

You’ve heard me talk about health plans, HSAs, and all the confusing alphabet soup that comes with insurance—but today we’re going to talk about the thing nobody wants to th ink about but absolutely needs to. Disability insurance. Yep, that “extra” benefit that people click past during enrollment like it’s spam—but listen, it’s anything but. 👉 And since May is Disability Insurance Awareness Month, there’s no better time to have this conversation. Because while most folks insure their phone, their car, and even that $200 air fryer they barely use, the one thing most of us forget to protect is the one thing we rely on the most: our income . Let me ask you something: If you woke up tomorrow and couldn’t work—how long would your savings last? (Go ahead. I’ll wait. It’s uncomfortable, I know.)

Let’s be real: mental health deserves more than just inspirational quotes and lavender-scented bath bombs. May is Mental Health Awareness Month , and while awareness is a great starting point, access is the real game-changer. That’s where insurance comes in—and no, not just the kind that covers an annual checkup and sends you on your way. If you're an employer, employee, or just a human being navigating life—mental health benefits matter. Therapy, counseling, medication, virtual mental health platforms…these are lifelines, not luxuries. So what should your insurance be doing for your mental health? Here’s what to look for (and ask about) in your plan: ✅ Teletherapy coverage – Because sometimes the best place to cry it out is in your car, on Zoom, between errands. ✅ No (or low) copays for behavioral health – Therapy shouldn’t cost more than brunch. ✅ Mental health parity – Plans should treat mental health care the same way they treat physical health care. Legally. Yes, it’s a law. ✅ Employee Assistance Programs (EAPs) – Employers, these are low-cost or no-cost additions that can provide real support to your team. But what if you’re on Medicaid… or a high-deductible plan? Now here’s where it gets interesting. There are new, low-cost health memberships on the market designed to fill the gaps left by traditional coverage. These plans aren’t insurance in the usual sense—but they offer direct access to primary care, mental health therapy (yep, including virtual sessions), lab work, and prescription support, often for less than the price of a cell phone bill. Perfect for: ✔️ People on Medicaid who can’t find a therapist ✔️ Folks with high-deductible health plans who never meet the deductible ✔️ Employers who want to offer a mental health option without blowing the budget ✔️ Solopreneurs and freelancers who need care without complications I’ve done the homework, and I’ve found a few that are game-changers. Employers, listen up. Your benefits package can make or break your employee retention and productivity. Offering meaningful mental health coverage isn’t just the “right thing”—it’s smart business. Mental health days, coverage for therapists that actually take insurance, and destigmatizing the whole convo? That’s how you build a workplace people want to stay in. And to the individuals: You don’t have to figure this out alone. If you're unsure whether your plan covers therapy or if you feel like you're paying out of pocket way too much, I can help review your benefits and break it down without the jargon. 📝 P.S. : Want to upgrade your employee benefits or make sure you’re actually getting what you pay for? Hit reply or book a call with me . Let’s get you covered, mind and all. 🧠 Because mental health is health.

We clean the baseboards. We KonMari the closets. We even organize the junk drawer no one wants to claim. But there’s one thing most folks skip during spring cleaning— their insurance policies . Yep, those dusty old documents sitting in a file folder—or worse, buried in your inbox from five years ago. If you haven’t done a spring insurance review , now’s the time. Because insurance isn’t “set it and forget it.” It should grow and change with you. Let’s dig into three small insurance tweaks that can freshen up your finances—and maybe even save you thousands.

I hope this finds you well, grounded, and not too overwhelmed by adulting, inflation, or allergy meds that make you feel like you’re floating three feet off the ground. This week I want to shine a light on something most people ignore until it’s too late: Health Savings Accounts (HSAs). The IRS just dropped the 2026 limits, and before you yawn and swipe away, let me say this—if you like saving money and planning ahead, this info is worth five minutes of your time (and maybe a coffee refill). But first, a quick story... Real Talk: The First Time I Really Used My HSA When I opened my HSA years ago, I honestly thought it was a government trick. Like, “Sure, save money for healthcare—but only if you hit this weird deductible and cross a moat of fine print.” But then life did what life does—I got hit with an unexpected dental bill that insurance barely touched, and boom. My HSA came through like the unsung hero it is. No stress, no credit card swipe, just paid. That was the day I became an HSA evangelist. So let me break it down for you—the updates, the “why it matters,” and what to do next.

Before We get into it… April is Autism Awareness Month—but for so many of us, this isn’t a cause we wear on a T-shirt. It’s our everyday reality. As a mama to an autistic child, I’ve lived the late-night Googling, the IEP-induced headaches, and the “why didn’t anyone tell me this?!” moments. Balancing school systems and insurance? That’s a whole job—on top of the one you already have. So this month, I’m not here to throw buzzwords at you. I’m here to share what I wish someone handed me when I was just trying to keep up: real talk, useful info, and permission to exhale. If you’re parenting, caregiving, or just trying to figure this all out—I see you. Let’s untangle the chaos, together.

Before We get into it… April is Autism Awareness Month—but for so many of us, this isn’t a cause we wear on a T-shirt. It’s our everyday reality. As a mama to an autistic child, I’ve lived the late-night Googling, the IEP-induced headaches, and the “why didn’t anyone tell me this?!” moments. Balancing school systems and insurance? That’s a whole job—on top of the one you already have. So this month, I’m not here to throw buzzwords at you. I’m here to share what I wish someone handed me when I was just trying to keep up: real talk, useful info, and permission to exhale. If you’re parenting, caregiving, or just trying to figure this all out—I see you. Let’s untangle the chaos, together.

Before We get into it… April is Autism Awareness Month—but for so many of us, this isn’t a cause we wear on a T-shirt. It’s our everyday reality. As a mama to an autistic child, I’ve lived the late-night Googling, the IEP-induced headaches, and the “why didn’t anyone tell me this?!” moments. Balancing school systems and insurance? That’s a whole job—on top of the one you already have. So this month, I’m not here to throw buzzwords at you. I’m here to share what I wish someone handed me when I was just trying to keep up: real talk, useful info, and permission to exhale. If you’re parenting, caregiving, or just trying to figure this all out—I see you. Let’s untangle the chaos, together.

Before We get into it… April is Autism Awareness Month—but for so many of us, this isn’t a cause we wear on a T-shirt. It’s our everyday reality. As a mama to an autistic child, I’ve lived the late-night Googling, the IEP-induced headaches, and the “why didn’t anyone tell me this?!” moments. Balancing school systems and insurance? That’s a whole job—on top of the one you already have. So this month, I’m not here to throw buzzwords at you. I’m here to share what I wish someone handed me when I was just trying to keep up: real talk, useful info, and permission to exhale. If you’re parenting, caregiving, or just trying to figure this all out—I see you. Let’s untangle the chaos, together.

If you’ve ever tried to navigate insurance coverage for autism-related care , you already know—it’s a whole battle. Like, why does something so necessary come with so much paperwork, so many denials, and so many hoops to jump through? It’s giving “we don’t actually want you to use this coverage” energy. As a parent of a child on the spectrum, I’ve been there. And as someone who actually knows the insurance industry, I’m here to say: the system is unnecessarily hard, and it doesn’t have to be. So, let’s talk about what’s happening, why it’s so difficult, and how to make sure you’re getting every dollar of coverage your family is entitled to.

Nobody dreams about the day they’ll have to choose between COBRA and the Marketplace . It’s not a fun decision. It’s not even a cute one. It’s a “Welp, I guess I’m the adult in the room now” kind of situation. And if you’ve recently lost your job — or you’re helping someone who has — this choice is probably staring you down. But don’t worry. I’m going to break it all down. With clarity , compassion , and just a little side-eye … Because the insurance system? Yeah, it stays doing the most. 🐍 Option 1: COBRA – The “Stay Where You Are” Plan COBRA (yep, it sounds like a Marvel villain) lets you keep the exact same health plan you had at work. Same doctors, same coverage, same everything. Sounds great — until the bill shows up. “Oh, you wanna keep your plan? That’ll be $1,500 a month. Plus a 2% admin fee. Love ya, mean it.” ✅ The Good: You already know the doctors, the coverage, and the drama No paperwork chaos — zero learning curve ❌ The Bad: It’s like buying a luxury car in cash… every month No financial help. You’re footing the entire premium solo 💻 Option 2: The Marketplace – The “Let’s Shop Around” Plan Also known as Healthcare.gov , the Marketplace is where you can browse and compare ACA-compliant plans — and possibly get a major discount if your income qualifies. Yes, the site can feel like a maze. Yes, it can be confusing. But if you push through the fog? You might save serious 💰. ✅ The Good: Real chance to pay a lot less with subsidies More plan options (Bronze, Silver, Gold — it’s giving Olympic Games) ❌ The Bad: You might need to switch doctors or adapt to a new network Shopping can feel overwhelming without guidance 👩🏽💼 Option 3: Small Group Plans – Even a “Group of One” Can Win If you’re a small business owner — even if it’s just you and your laptop — you might qualify for a small group health plan . Yes, a group of one is a real thing. Wild, right? 💡 Why it’s worth looking into: If you don’t qualify for subsidies, small group rates are often 15–30% cheaper than individual Marketplace plans These plans often come with broader networks and richer benefits You’ll need an EIN and to meet a few basic criteria, but if you qualify? This option can seriously stretch your dollars 🎯 Option 4: GigCare – The “Built for Freelancers” Plan Now for the option most people haven’t heard of — GigCare . If you’re freelancing, consulting, ridesharing, creating, or otherwise living that 1099 hustle , this might be your best-kept secret. GigCare is a fully ACA-compliant , traditional health insurance plan built for independent workers . 🧬 How GigCare Works (Without the Headache) Think of it like a level-funded health plan , where you join a group pool of other gig workers. That shared structure helps keep premiums more affordable — without skimping on real coverage. ✅ What Makes It Different: It’s underwritten : You’ll answer a few health questions to qualify. It’s not guaranteed issue like the Marketplace — but that’s how they keep costs down. Preventive care is 100% covered — physicals, mammograms, vaccines, screenings. It’s legit : GigCare follows all ACA rules and includes all 10 essential health benefits. This isn’t a discount card or sketchy “limited” plan. It’s real insurance , designed for people without a traditional employer plan who still want protection and peace of mind. 📞 Need Help Choosing? This is literally what I do. If you’re overwhelmed, confused, or just want someone to walk you through it, let’s chat. 🎯 Book a 15-min strategy call 📤 Or forward this post to someone who needs to know: they’ve got more than two options. Because adulting is hard enough — your insurance decision doesn’t have to be. 🧠 FAQs Q: What’s the difference between COBRA and the Marketplace? A: COBRA lets you keep your old job-based plan, but you pay the full cost. The Marketplace offers new ACA plans — often with financial help based on income. Q: What’s the cheapest option if I just lost my job? A: If your income drops, the Marketplace can be very affordable with subsidies. If you don’t qualify, small group or GigCare plans are often cheaper than COBRA. Q: Can freelancers really get group health insurance? A: Yes! If you have an EIN and meet a few basic criteria, you can qualify for a small group plan — even as a “group of one.” Q: Is GigCare legit insurance? A: 100%. It’s ACA-compliant, covers preventive care, and includes all essential benefits. It’s just tailored for independent workers. Q: Do I need a broker to help with this? A: Technically, no. But if you don’t want to overpay, miss key deadlines, or get stuck with the wrong coverage? Then yes — that’s where I come in. I make the process painless and personalized. – Carmen Still out here Covering Your ASSets with heart, hustle, and real insurance guidance. 📍 www.insurepros.net

Listen, we get it—insurance isn’t exactly the first thing you want to deal with in the new year. But trust us, it’s about to be the easiest thing you check off your list in 2025. Here at The Insurance Pros, we’re more than policies and paperwork; we’re your go-to for peace of mind and confidence that your people, your home, your everything are covered. Here’s how we’re showing up this year to make insurance a breeze: 1. Clarity in Coverage You know how insurance feels like a foreign language? Like, “Am I supposed to have a dictionary for this?” We’re not doing that anymore. In 2025, we’re putting the fine print on blast and making sure you actually understand your coverage. No guessing. No confusion. Just straightforward info about what’s covered, what’s not, and what’s next. For real, when you sit down with us, you’ll leave knowing exactly how your policy protects you and your family. Because insurance isn’t supposed to make you feel like you’re solving a Rubik’s Cube. 2. Enhanced Client Education Let’s be honest: when it comes to insurance, the more you know, the less you panic. That’s why 2025 is the year we’re stepping up our education game. Think blogs that break it all down, videos that don’t bore you to tears, and myth-busting that makes you go, “Wait… I didn’t know that.” We’re also launching a newsletter! Want exclusive tips, updates, and answers to your burning insurance questions delivered straight to your inbox? Head over to our Contact Us page to sign up for our emails. Staying informed has never been easier. And that’s not all—we’re bringing even more helpful info to our social media. Follow us for practical advice, timely updates, and a little humor to brighten your day. Insurance doesn’t have to be dull, and we’re here to prove it. 3. Community Connection We’re not just the folks you call for insurance; we’re part of your neighborhood. This year, we’re getting out there and showing up for our communities. Local events? We’ll be there. Supporting initiatives that make life better for you and yours? Count us in. 2025 is about building connections that matter—and not just in business. Whether it’s sharing resources or helping families get the protection they need, we’re here for you. 4. Stress-Free Service Life’s already stressful enough. The last thing you need is your insurance giving you a headache. That’s why we’re making everything smoother—from policy reviews to claims to renewals. Simple. Quick. Done. We’ve got new tools coming your way, like a client portal and automated reminders, so you can stay on top of your coverage without lifting a finger. When we say “stress-free insurance,” we mean it. We Want to Hear from You What are your 2025 goals? Protecting your family? Growing your business? Finally getting your insurance in order? Whatever it is, we’re here to help make it happen. We’re inviting you to share your goals with us. How can we support you this year? Whether it’s personalized advice or just being there when you need us, we’re ready to partner with you every step of the way. Here’s to a Great Year Ahead 2025 is a new chapter, and we’re so grateful to be part of your story. Thank you for trusting us with what matters most. At The Insurance Pros, we’re ready to help you navigate whatever comes next—with confidence, clarity, and zero drama. Here’s to a year of protection, peace of mind, and progress—together.

As the holiday season approaches, we at The Insurance Pros (TIP) want to extend our warmest wishes to our cherished clients and partners. Reflecting on the past year, we're filled with gratitude for the trust you've placed in us and the milestones we've achieved together. This year, we expanded our comprehensive insurance solutions, ensuring that your life, assets, and peace of mind remain our top priorities. From personalized home and auto coverage to tailored business insurance plans, we've been dedicated to providing protection that truly works when life gets real. A highlight of 2024 was our commitment to assisting small and micro businesses in entering the group market. We introduced options like One Person Group plans, allowing business owners to secure quality coverage for themselves or retain that rockstar employee in need of better benefits. As we look forward to 2025, we're excited to continue offering insurance made clear and protection made simple. Your support has been instrumental in our success, and we're eager to keep delivering the reliable and affordable coverage you deserve. ✨ From all of us at TIP, may your holidays be filled with joy, and may the new year bring you health, happiness, and prosperity. Here's to another year of protecting what matters most! Call to Action: As we gear up for another amazing year, let us be your go-to for all things insurance. Whether it's protecting your home, business, or future, we're here to make coverage clear and hassle-free. Visit insurepros.net to explore how we can help you start 2025 with confidence! 💼📞

Carmen shares her go-to sofrito recipe, the flavorful base that brings depth and richness to so many Latin dishes.

Dr. José Celso Barbosa, a man who was out here in the 1800s breaking molds and making history. When we say “trailblazer,” we mean it! Born on July 27, 1857, Barbosa wasn’t just the first Black Puerto Rican to practice medicine in Puerto Rico—he was one of the first Black men to earn a medical degree in the U.S., period. He didn’t just break down doors; he paved a whole highway for generations after him, from medical innovation to political activism and even inventing a little thing we now call “employer-based health insurance.” Yes, he did that too. Schooling and Straight-Up Determination: A Role Model for the Ages Barbosa’s journey to becoming a doctor? Not for the faint-hearted. This was the late 19th century, where being Black, Puerto Rican, and ambitious enough to attend the University of Michigan for medical school was unheard of. But Barbosa wasn’t about to let anything stop him. He graduated in 1880, kicking down barriers and showing other Hispanic and Black folks that medicine, too, could be their calling. This man’s hustle didn’t just make him a doctor—it made him a beacon for everyone dreaming bigger than the world thought they could. Employer-Based Health Insurance? Yeah, He Was That Visionary Barbosa didn’t just want to be any doctor; he wanted to make healthcare work for the people. When he got back to Puerto Rico, he looked around and saw the healthcare crisis brewing for low-income families. So, what did he do? He set up a mutual aid system, asking people to contribute a small monthly fee to cover their healthcare costs when needed. Yup, he practically invented employer-based health insurance right there in Puerto Rico. It was revolutionary. Quality healthcare, he believed, shouldn’t be a luxury; it’s a right. This man was doing 21st-century things in the 1800s! Politics and the Fight for Puerto Rican Autonomy Now, as if medicine and employer-based health insurance weren’t enough, Barbosa decided to jump into politics. In 1899, he started the Puerto Rican Republican Party, giving Puerto Ricans a voice and demanding equal representation. He was all about empowering his people, and his political legacy is still a blueprint for leaders fighting for Puerto Rican rights today. Barbosa was about Puerto Rican dignity, identity, and autonomy, and he wasn’t afraid to challenge power structures to make that happen. Honoring Dr. Barbosa During Hispanic Heritage Month Dr. José Celso Barbosa didn’t just live a life; he made history. He’s what Hispanic Heritage Month is all about—honoring those who paved the way, lifted communities, and demanded better for everyone around them. Barbosa’s legacy is proof of the power of pushing boundaries and standing up for what’s right, even when the world isn’t ready. This month, we celebrate his work, his courage, and his relentless pursuit of justice. Let his story remind us to keep fighting, keep dreaming, and always keep looking out for each other.

In celebration of #HispanicHeritageMonth , I’m sharing a special recipe each week that’s close to my heart! First up is my Feta & Fire-Roasted Salad —a flavorful dish packed with tangy feta and smoky roasted veggies. It's one of my personal favorites!

It’s Q4! Time to get smart about your health coverage. New plans, better networks, and some serious savings are up for grabs. Don’t let this opportunity pass you by—let’s break down how The Insurance Pros can help you lock in the best plan for your wallet and your health!

Hey there! Gather 'round, because we’re about to dive into immunization coverage in Illinois health insurance plans. Whether you're a vaccine enthusiast or a bit hesitant, this info is going to make you smarter and ready to navigate that insurance maze like a pro. Why Immunizations Matter First, let’s talk about why immunizations are a big deal. Immunizations play a crucial role in keeping you alive and kicking. They protect you from a whole range of nasty diseases that can seriously mess with your health. From the time you’re a baby to when you’re all grown up, these shots keep you safe and healthy. Plus, staying up-to-date with your vaccines means you’ll recover faster if you do get sick, and it helps protect the people around you too. It's about building a strong defense for you and your community. What’s Covered? Alright, now let’s dive into what your health insurance in Illinois covers when it comes to immunizations. Most health plans have to cover a bunch of vaccines without making you pay out-of-pocket. That’s thanks to the Affordable Care Act (ACA). Here’s a quick rundown of some shots that are usually covered: Kids: Chickenpox , measles, mumps, rubella (MMR) , polio , whooping cough (pertussis) , and more. Teens: HPV , meningococcal , and Tdap (tetanus, diphtheria, pertussis) . Adults: Flu shot , shingles (for those over 50), and pneumonia (for older folks or those with certain health conditions). Pretty cool, right? Your plan might cover even more, so it’s always a good idea to check with your provider. How to Make Sure You’re Covered You don’t want surprises when it's time for your shot. Here’s how to make sure you’re covered: Check Your Plan: Go through your health insurance policy or give them a call to see exactly what’s covered. In-Network Providers: Make sure you’re going to a doctor or clinic that’s in your insurance network. Going out-of-network could mean you’ll end up paying more. Stay Informed: Keep track of your immunization schedule. If you’re unsure about what vaccines you need, don’t be shy—ask your doctor! The CDC’s immunization schedule is a great resource. What If You’re Uninsured? No insurance? No problem. Illinois has got your back. Programs and local health departments can help you get vaccinated at little or no cost. It’s all about keeping everyone in our community healthy. A few are listed here- Vaccines for Children (VFC) Program Provides free vaccines to eligible children. Learn more: CDC’s VFC Program . Illinois Department of Public Health (IDPH) Offers immunization services statewide. Learn more: IDPH Immunization Page . Federally Qualified Health Centers (FQHCs) Provides immunizations on a sliding fee scale. Find a center near you: IPHCA . Local Health Departments Many local health departments provide low-cost vaccines. Locate yours: IDPH Directory . Chicago Department of Public Health (CDPH) Provides free and low-cost vaccines through city clinics. Learn more: CDPH Immunization Program . Ready to take charge of your health? Immunizations are key to keeping you and your community safe and healthy. Don’t wait—check your health insurance plan today to see what’s covered, make sure you’re visiting in-network providers, and stay informed with the CDC’s immunization schedule. Let's roll up those sleeves and stay protected! Call us now and keep your immunizations up-to-date. Your health matters, and staying on top of your vaccines is a powerful step towards a healthier future for you and those around you. Stay healthy, stay informed, and keep that immune system ready for anything!

Introduction Alright, friends, it’s that time of year again—Open Enrollment. Just hearing those words might make you want to hide under your covers, but don’t worry, I’m here to make sure you’re ready to face it head-on. Whether you’re a newbie or a seasoned vet, there’s always something new to learn when it comes to health insurance, and this year is no different. We’re going to break it down so you’re not out here making guesses with your health coverage. By the end of this blog, you’ll feel like a health insurance ninja, ready to take on Open Enrollment like a pro. And the best part? The Insurance Pros are here to guide you every step of the way. What is Open Enrollment? Let’s start with the basics: what exactly is Open Enrollment? Think of it as your annual opportunity to review, change, or enroll in a health insurance plan. Whether you’re looking to join a new plan, switch up your coverage, or stay where you are, this is your window of time to make those decisions. But here’s the catch—it’s a limited-time offer, my friends. The clock is ticking from November 1 to January 15, so you’ve got to make moves before the deadline passes. The good news? The Insurance Pros are ready to help you navigate this crucial period, ensuring you’re set up with the best possible coverage for the year ahead. Key Dates to Remember: GRAPHIC WITH DATES Mark those dates on your calendar, set a reminder on your phone—do whatever it takes to ensure you don’t miss this window. Trust me, you don’t want to be scrambling at the last minute. Decoding Insurance Terms Okay, now that we’ve got the basics out of the way, let’s talk about the language of health insurance. If you’re like most people, terms like “premium,” “deductible,” and “copayment” might as well be written in ancient hieroglyphics. But don’t worry, I’ve got you covered. Premium: This is what you pay each month just to have health insurance. Think of it like a subscription fee. Whether you use your insurance or not, this amount is coming out of your bank account. Deductible: This is the amount you have to pay out of your own pocket before your insurance starts kicking in. If your deductible is $1,000, you’ll need to pay that much in medical costs before your insurance starts to cover the bills. Copayment: This is a fixed amount you pay for a covered service, like a doctor’s visit or prescription. It’s your share of the cost, and it’s usually pretty small—think $20 or $30 per visit. Understanding these terms is crucial because they directly affect your wallet. The Insurance Pros can break down these costs for you, helping you understand what you’ll be paying and when, so there are no surprises down the road. Why Open Enrollment is Crucial Now, let’s talk about why Open Enrollment is such a big deal. Life doesn’t stay the same, and neither should your health insurance. Maybe you got married, had a baby, or changed jobs—these are all major life events that can impact your coverage needs. Open Enrollment is your chance to review your current plan and make sure it still fits your life. Not participating in Open Enrollment means you might be stuck with a plan that doesn’t work for you, or worse, you could face penalties if you’re uninsured. It’s not just about picking a plan; it’s about making sure you have the coverage you need to stay healthy and protected. The Insurance Pros are here to ensure you don’t miss out on this opportunity. They’ll help you assess your current situation, identify any gaps in coverage, and find a plan that meets your needs. Conclusion So, what have we learned today? Open Enrollment is your yearly chance to make sure your health insurance is working for you. It’s a limited window, so you’ve got to act fast. But don’t worry—you don’t have to do it alone. The Insurance Pros are ready to help you navigate the process, break down the confusing jargon, and find the perfect plan for you. Whether you’re looking to switch things up or stick with what you’ve got, they’ve got your back. Don’t let Open Enrollment pass you by—reach out to The Insurance Pros today and make sure you’re covered for 2025.

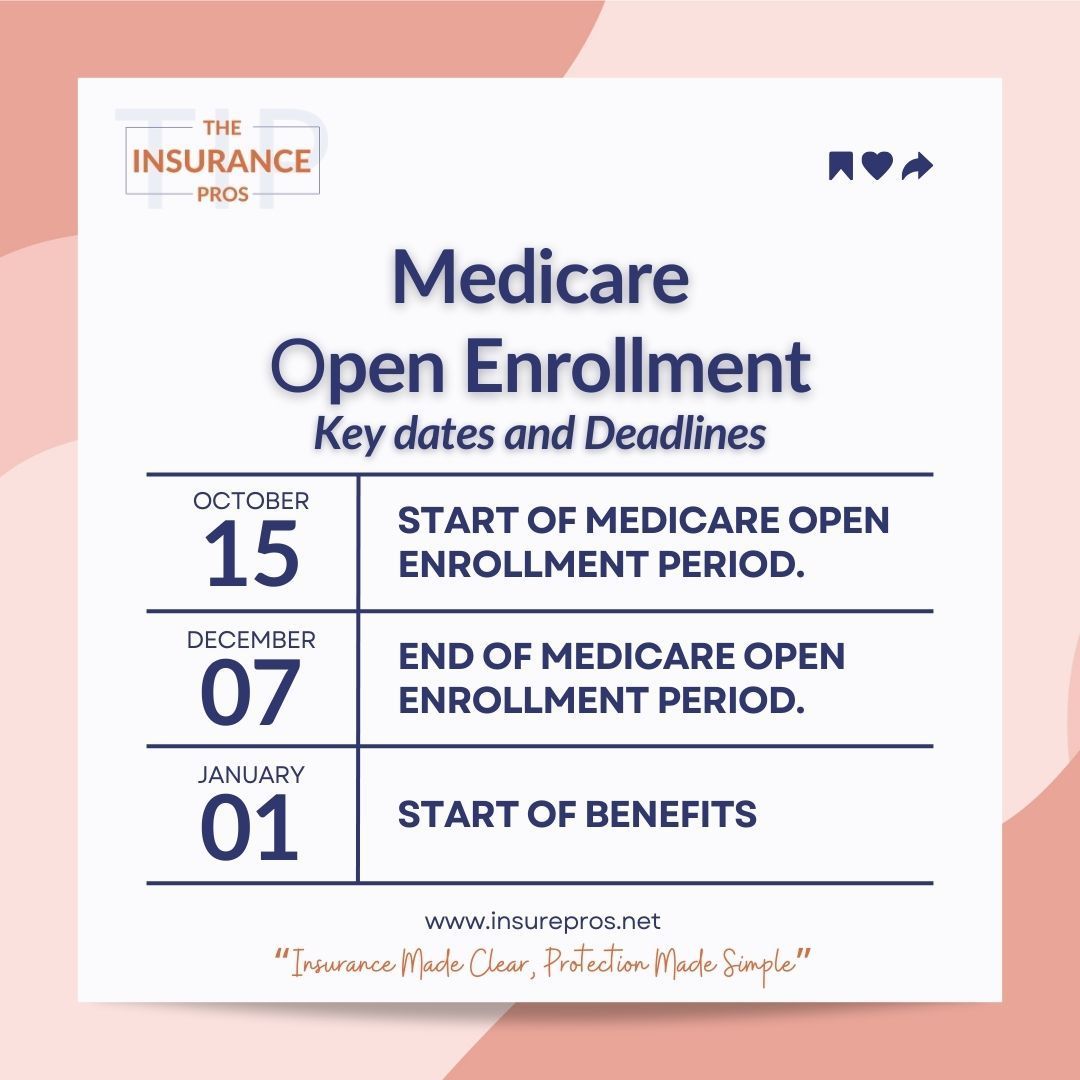

Introduction: The 2024 Medicare Open Enrollment season is right around the corner—October 15 to December 7, to be exact. This is your golden opportunity to review your Medicare coverage and make any changes necessary to ensure you’re getting the most out of your plan. Whether you need to switch from Original Medicare to a Medicare Advantage plan, join a new drug plan, or just update your coverage, this is the time to do it. But don’t worry, The Insurance Pros are here to help you navigate these changes and make the best decision for your healthcare needs. Key Updates in 2025: Prescription Drug Coverage: This year, there are significant changes in Medicare Part D prescription drug coverage. With new caps on insulin costs and out-of-pocket expenses, you could save a lot—if you’re on the right plan. The Insurance Pros can review your current plan and compare it with new options, ensuring you’re not missing out on these potential savings. Telehealth Services: Telehealth is here to stay, and Medicare is expanding its coverage for these services. But not all plans are created equal when it comes to telehealth. The Insurance Pros can guide you through the maze of options to find a plan that gives you the flexibility to consult with your healthcare provider from the comfort of your home. New Plan Options: 2024 brings several new Medicare Advantage plans with unique benefits like fitness programs, transportation services, and more. With so many options, it can be overwhelming to figure out which one is right for you. The Insurance Pros will help you sift through the details, comparing benefits, costs, and network coverage to find the perfect fit for your needs. Enrollment Period Insights: Remember, you can make these changes between October 15 and December 7. You can join, drop, or switch to a Medicare Advantage plan, switch from Original Medicare to Medicare Advantage, or switch from one Medicare drug plan to another. You can also update your coverage by switching to a new plan from your current insurer or by choosing a new insurer altogether. And if you’re under 65 and receive Social Security or Railroad Retirement Board benefits, you might be automatically enrolled in Original Medicare. Plus, if you need to make any changes during the Medicare Advantage Open Enrollment period, you have from January 1 to March 31 to do so, with your new plan benefits taking effect for the rest of the year. How The Insurance Pros Can Help: Navigating these changes can be overwhelming, but The Insurance Pros are here to help. They stay up-to-date with the latest changes and trends, so you don’t have to. Whether you need help understanding new benefits, comparing plans, or just want someone to explain what all these changes mean for you personally, The Insurance Pros are your go-to resource. They’ll make sure you’re fully informed and confidently enrolled in the best plan for 2024.

Hey, guys! Let's have a little chat about something super important—your health. Yep, I know it’s not the most exciting topic, but trust me, it’s worth a few minutes of your time. Whether you’re hitting the gym, playing a weekend game of basketball, or just trying to keep up with the kids, taking care of your health is key. And having the right insurance can make a world of difference. So, let’s dive into some essential coverage tips for men in Illinois. Ready? Let’s go! Why Men’s Health Matters Before we get into the nitty-gritty of insurance, let’s talk about why your health matters. Men often skip regular check-ups and ignore symptoms, but early detection and prevention are crucial. Regular health screenings can catch issues before they become serious, and having the right insurance ensures you get the care you need without breaking the bank. Common Health Concerns for Men Heart Disease: The leading cause of death for men in the U.S. Regular screenings and lifestyle changes can help manage and prevent heart disease. Cancer: Prostate, lung, and colorectal cancers are among the most common. Early detection through screenings can significantly improve treatment outcomes. Diabetes: A growing concern for many men, especially those with a family history. Regular screenings can help manage and prevent diabetes. Mental Health: Depression and anxiety are common but often overlooked. Mental health is just as important as physical health and should be treated with equal importance. Respiratory Diseases: Conditions like chronic obstructive pulmonary disease (COPD) are common, especially in smokers. Early detection and treatment are vital. Reproductive Health: Issues like low testosterone, erectile dysfunction, and prostate problems are common. Regular check-ups and open conversations with your doctor can help manage these concerns. Must-Have Insurance Coverage Routine Check-Ups and Preventive Care: Regular visits to your primary care physician are essential. Preventive care includes screenings for blood pressure, cholesterol, diabetes, and certain cancers. Make sure your insurance covers these routine visits and tests. Many preventive services are federally mandated to be free or covered 100%, so no excuses! Specialist Visits: Sometimes you need to see a specialist—whether it’s for your heart, joints, or another issue. Ensure your insurance plan includes specialist visits without needing excessive referrals or jumping through hoops. Mental Health Coverage: Mental health is just as important as physical health. Look for a plan that offers mental health services, including therapy and counseling, without high out-of-pocket costs. Prescription Coverage: If you need medication, having good prescription coverage is a must. Check if your plan covers both generic and brand-name drugs and what the co-pays look like. Emergency and Hospital Care: Accidents happen. Make sure your plan covers emergency room visits and hospital stays. It’s better to be safe than sorry! Key Screenings and Tests for Men Taking care of your health means getting the right screenings at the right times. Here’s a rundown of essential screenings for men, and remember, many of these are federally mandated to be free or covered 100%: Blood Pressure Screening When: Starting at age 18, at least once every two years. Coverage: Federally mandated to be free. Cholesterol Check When: Starting at age 20, every 4-6 years. Coverage: Federally mandated to be free. Diabetes Screening When: Starting at age 45, every 3 years. Coverage: Federally mandated to be free. Colorectal Cancer Screening (Colonoscopy) When: Starting at age 50, every 10 years, or earlier and more frequently if you have a family history of colorectal cancer. Coverage: Federally mandated to be free. Prostate Cancer Screening When: Starting at age 50, or 40-45 if you have a family history. Coverage: Check with your insurer, as coverage can vary. Skin Cancer Screening When: Annually, especially if you have a history of sunburns or family history. Coverage: Often covered, but check with your insurer. Mental Health Screening When: Annually, or as needed. Coverage: Federally mandated to be free. Reproductive Health Screening When: Regularly, especially if experiencing symptoms like low libido or erectile dysfunction. Coverage: Often covered, but check with your insurer. Tips for Choosing the Right Plan Know Your Health Needs: Are you someone who rarely gets sick, or do you have a chronic condition that requires regular care? Choose a plan that fits your lifestyle and health needs. Check the Network: Make sure your preferred doctors and hospitals are in-network. Out-of-network care can be significantly more expensive. Consider the Costs: Look at the premiums, deductibles, co-pays, and out-of-pocket maximums. Sometimes a higher premium plan with lower out-of-pocket costs is better if you need frequent care. Look for Added Benefits: Some plans offer perks like gym memberships, wellness programs, or telehealth services. These can be great additions to your health routine. Read the Fine Print: Understand what is and isn’t covered. Some plans may have limitations or require prior authorizations for certain services. Insurance Options in Illinois Living in Illinois, you have several insurance options, whether you’re employed, self-employed, or looking for coverage on your own. Here are a few: Employer-Sponsored Plans: If you’re employed, check out the health plans offered by your employer. These often come with lower premiums due to group rates. Marketplace Plans: The Health Insurance Marketplace offers various plans, and you might qualify for subsidies based on your income. Medicaid: If you meet certain income requirements, you might be eligible for Medicaid. This provides comprehensive coverage at little to no cost. Private Insurance: For those who want more control over their plans, private insurance is an option. Compare different plans and providers to find the best fit. Take Action Today Your health is your most valuable asset. Don’t wait until something goes wrong to think about insurance. Review your current coverage, see where you might need more protection, and make sure you’re getting the best possible care. If you’re unsure about where to start, reach out to an insurance agent—they’re there to help you navigate the options and find the best plan for your needs. Call to Action Ready to level up your health game? Contact us at Insurance Pros for a personalized consultation. We’ll help you find the best insurance coverage to keep you healthy and thriving. Visit our website or give us a call today! Here’s to taking charge of your health and living your best life! 💪

Hey, business owners! Summer is here, and if you’re in Chicago or anywhere in the Midwest, you know this season is all about bustling streets, festivals, and tourists galore. Whether you’re running a lakeside café, a landscaping service, or a boutique hotel, the summer rush can bring both excitement and challenges. One thing you definitely don’t want to overlook is your business insurance. Let’s dive into why seasonal business insurance is a must and how to get your business ready for the sunny months ahead. What is Seasonal Business Insurance? First things first, what exactly is seasonal business insurance? It’s a type of insurance designed specifically for businesses that experience significant fluctuations in activity throughout the year. Think of it as tailored coverage that ramps up when you’re busiest and scales back when things are slower. It’s all about having the right protection at the right time. Why You Need It Let’s be real, the summer rush can be a rollercoaster. Here’s why seasonal business insurance is crucial: Increased Liability: With more customers, there’s a higher chance of accidents and injuries. Whether it’s a slip-and-fall at your ice cream stand in Navy Pier or a mishap on your boat rental at Lake Michigan, you need coverage that can handle the increased liability. Property Protection: Summer often means more inventory, equipment, and cash on hand. Seasonal insurance ensures your property is protected against theft, damage, or loss during peak times. Employee Coverage: If you’re hiring seasonal staff, make sure they’re covered. Workers’ compensation and liability insurance are essential to protect both your employees and your business. Business Interruption: Summer storms, power outages, or unexpected events can disrupt your operations. Business interruption insurance can help cover lost income and ongoing expenses if you have to close temporarily. Benefits of Seasonal Business Insurance Cost-Effective: Seasonal insurance can be more affordable than year-round coverage. You pay for the protection you need when you need it, without over-insuring during slower periods. Flexible Coverage: Customize your policy to match the unique risks and needs of your business during peak season. It’s like having a safety net that adapts to your business cycles. Peace of Mind: Knowing you’re covered allows you to focus on running your business and serving your customers without worrying about unexpected setbacks. Preparing Your Business for the Summer Rush Now that we’ve covered why seasonal business insurance is essential, let’s talk about getting ready for the summer surge: Review Your Current Policy: Take a close look at your existing insurance policy. Are there gaps in coverage that could leave you vulnerable during peak season? It might be time for an update. Assess Your Risks: Consider the specific risks your business faces in the summer. Are you prepared for increased foot traffic, more transactions, or outdoor events? Make sure your insurance covers these scenarios. Inventory Check: Conduct a thorough inventory check. Ensure you have adequate coverage for all your stock and equipment, especially if you’re ramping up for the season. Hire Smart: If you’re bringing on seasonal workers, make sure they’re properly trained and aware of safety protocols. Confirm they’re covered under your workers’ compensation policy. Plan for the Unexpected: Have a contingency plan in place for potential disruptions. Whether it’s a natural disaster or a supply chain issue, being prepared can make all the difference. Real-Life Example Let’s look at a real-life example. Jenny owns a popular café in Chicago’s bustling downtown area. Last summer, a sudden storm caused significant damage to her outdoor seating area. Fortunately, Jenny had seasonal business insurance that covered the repair costs and business interruption. She was able to reopen quickly and continue serving her customers without a hitch. Conclusion The summer rush in Chicago and the Midwest is an exciting time for many businesses, but it also comes with its own set of challenges. Seasonal business insurance is your best ally in navigating these busy months with confidence. By ensuring you have the right coverage, you can protect your business, employees, and customers, and enjoy a successful summer season. Call to Action Ready to get your business summer-ready? Contact us at Insurance Pros for a free consultation and find the perfect seasonal business insurance plan for your needs. Visit our website or give us a call—we’re here to help you thrive this summer! So, gear up and get covered. Let’s make this summer your best one yet, with all the fun and none of the worries. Here’s to a sunny, successful season! 🌞🏖️

Hey there, Gen Xers and Millennials! I know, I know—long-term care insurance might not be at the top of your priority list. Between juggling careers, family, and maybe even some TikTok time, thinking about long-term care can feel like something for way down the road. But here’s the thing: planning now can save you a lot of stress (and money) later. So, grab your favorite drink, get comfy, and let’s chat about why you should start caring about long-term care insurance today. What is Long-Term Care Insurance? First things first, what exactly is long-term care insurance? It’s a type of insurance designed to cover the costs of long-term care services, which aren’t typically covered by regular health insurance or Medicare. This can include help with daily activities like bathing, dressing, and eating, whether at home, in a community setting, or in a nursing home. Think of it as a safety net for your future self. Why Should Gen X and Millennials Care? Let’s be real for a second—thinking about needing long-term care isn’t exactly a fun topic. But here’s why it matters: Costs Can Be Astronomical: Long-term care is expensive. In fact, the average cost of a private room in a nursing home is over $100,000 per year. Without insurance, these costs can quickly drain your savings and impact your family’s financial security. Family Impact: Many of us expect family members to step in and help out, but providing long-term care can be physically, emotionally, and financially draining for loved ones. Having insurance can alleviate some of this burden. Early Planning = Lower Costs: The younger you are when you purchase long-term care insurance, the lower your premiums will be. Waiting until you’re older can significantly increase costs, and you might also face health issues that make it harder to get coverage. Increasing Life Expectancy: We’re living longer than ever, which means more years where we might need a little extra help. Planning now ensures you’re prepared for the long haul. Benefits of Long-Term Care Insurance So, what’s in it for you? Here are some key benefits of having long-term care insurance: Financial Protection: Protect your savings and assets from the high costs of long-term care services. Choice of Care: Insurance gives you more options when it comes to choosing the type of care you receive and where you receive it. Peace of Mind: Knowing you’re covered allows you to focus on enjoying life without worrying about the “what ifs.” Support for Family: Reduce the emotional and financial strain on your family by ensuring they won’t have to bear the full burden of your care. How to Get Started Ready to start planning? Here are some steps to get you on your way: Assess Your Needs: Think about your family health history and lifestyle. Do you have a history of chronic illnesses? Do you lead a healthy, active lifestyle? Research Policies: Not all long-term care insurance policies are the same. Look at different options, compare benefits, and check out customer reviews. Talk to an Expert: Reach out to an insurance professional who can help guide you through the process and find a policy that fits your needs and budget. Plan Early: Remember, the earlier you start, the better. Don’t wait until you’re older and premiums are higher. Questions to Ask an Agent When you’re ready to talk to an insurance agent, here are some questions to help you get the best coverage: What Does the Policy Cover? Make sure you understand exactly what services and types of care are included in the policy. What Are the Exclusions? Know what is not covered to avoid any surprises down the road. What Are the Premiums and How Do They Increase Over Time? Get a clear picture of your financial commitment now and in the future. Is There an Inflation Protection Option? This can help your benefits keep pace with rising costs over time. What Are the Eligibility Requirements for Benefits? Understand what conditions must be met to start receiving benefits. Are There Any Discounts Available? Ask about any discounts for healthy living, joint policies, or other factors. What Are the Payment Options? Find out if you can pay monthly, quarterly, or annually, and if there are any benefits to each option. How Long Are the Benefits Paid? Check the duration of the coverage to ensure it meets your potential needs. Can the Policy Be Customized? See if you can tailor the policy to better fit your personal situation and future needs. Conclusion Long-term care insurance might not be the most exciting thing to think about, but it’s one of the smartest moves you can make for your future self. By planning now, you’re not just protecting your finances—you’re also giving yourself and your family the gift of peace of mind. So, why wait? Start exploring your options today and set yourself up for a worry-free future. Call to Action Ready to learn more about long-term care insurance? Contact us at Insurance Pros for a free consultation and let’s find the perfect plan for your needs. Visit our website or give us a call—we’re here to help you every step of the way. Here’s to planning smart and living well! 🌟

Hey there, summer’s almost here! 🌞 That means it’s time for sunshine, beach days, and exciting travel plans. Whether you’re jetting off to a tropical paradise or taking a road trip across Illinois, you’ve probably been daydreaming about your perfect getaway. But before you pack your bags and grab your sunscreen, let’s chat about something that might not be on your radar—travel insurance. Yep, I know it’s not the most glamorous topic, but stick with me. It could save your vacation! What is Travel Insurance? Alright, so what exactly is travel insurance? Think of it as your safety net when you’re away from home. It’s designed to protect you from those “just in case” moments. You know, those unexpected things that can pop up and throw a wrench in your travel plans. Travel insurance can cover everything from trip cancellations and medical emergencies to lost luggage and travel delays. It’s like having a little guardian angel watching over your vacation. Why Consider Travel Insurance? Let’s get real for a second. Life happens, even when you’re on vacation. Here’s why travel insurance might be your new best friend: Unexpected Cancellations: Imagine you’ve planned the perfect trip, but then you get sick, or there’s a family emergency. Travel insurance can help you get your money back for those non-refundable expenses. Medical Emergencies: If you’re traveling abroad, your regular health insurance might not cover you. Travel insurance steps in to cover those unexpected medical bills. Because the last thing you want is to be stuck with a huge bill while trying to enjoy your trip. Lost or Delayed Luggage: We’ve all heard horror stories about lost luggage. Travel insurance can reimburse you for the essentials if your bags go missing or are delayed. No more stressing about your favorite outfits being stuck in transit. Travel Delays: Weather happens, flights get delayed, and connections get missed. Travel insurance can cover extra expenses like hotels and meals if you’re stuck somewhere unexpectedly. Benefits of Travel Insurance Now, let’s talk about the perks of having travel insurance: Peace of Mind: Knowing you’re covered for those “what if” moments lets you relax and enjoy your trip without worry. Financial Protection: Vacations can be a big investment. Travel insurance helps protect that investment, so you don’t lose out if something goes wrong. Assistance Services: Many travel insurance plans offer 24/7 assistance services. Need help finding a doctor or rebooking a flight? They’ve got your back. Considerations Before Purchasing Before you rush off to buy travel insurance, here are a few things to keep in mind: Evaluate Your Needs: Think about your travel plans and what kind of coverage makes sense for you. Are you going somewhere with high medical costs? Planning a pricey trip? Check Existing Coverage: Sometimes your credit card or health insurance might offer some travel coverage. Check what you already have so you don’t buy something you don’t need. Read the Fine Print: Not all travel insurance policies are created equal. Make sure you understand what’s covered and what’s not. You don’t want any surprises! Real-Life Examples Let’s hear from some real people who’ve been there: Casey’s Story: Casey was all set for a dream vacation in Europe when her flight got canceled due to a storm. Thanks to her travel insurance, she got reimbursed for her extra hotel nights and meals while she waited for the next flight. Alex’s Adventure: Alex fell while hiking in the mountains and needed emergency medical care. Her travel insurance covered the hospital bills, which would have been a huge hit to her savings otherwise. These stories are just a few examples of how travel insurance can turn a potential disaster into a minor hiccup. How to Choose the Right Travel Insurance Choosing the right travel insurance can feel overwhelming, but it doesn’t have to be: Compare Plans: Look at different plans and see what they offer. Don’t just go for the cheapest option—make sure it covers what you need. Consider the Destination: Some places have higher medical costs or different risks. Make sure your plan fits your destination. Ask Questions: Don’t be shy! Ask insurers about coverage limits, exclusions, and how to make a claim. It’s better to know upfront. Let’s Wrap It Up So, do you really need travel insurance? If you want peace of mind, financial protection, and a safety net for those unexpected moments, the answer is a resounding yes. As you plan your summer adventures, consider adding travel insurance to your checklist. It might just be the best decision you make for your vacation. Call to Action Ready to make your travel plans worry-free? Contact us today for a free consultation and get a travel insurance quote tailored to your needs. Visit our website or give us a call—we’re here to help you travel smart and stay safe. So there you have it! Travel insurance might not be glamorous, but it’s your vacation’s best friend. Let’s make sure your summer adventures are all fun and no fuss. Happy travels! ✈️🌴

It’s Mental Health Awareness Month: Let’s Get Real About Your Insurance Coverage!